By Thierry Hasse, Chief Investment Officer

Elevage Partners | May 14, 2026

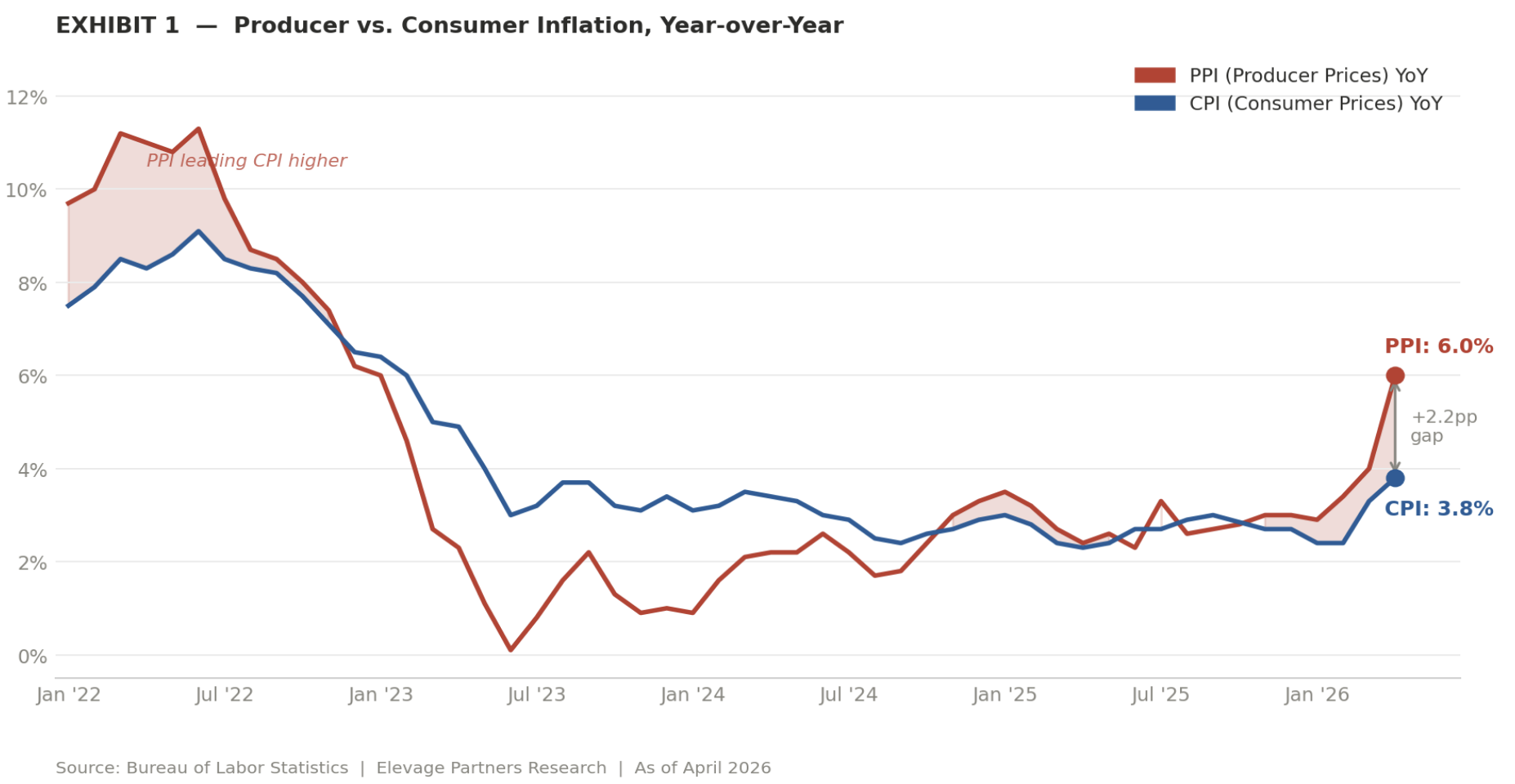

The Producer Price Index (PPI) report didn’t arrive quietly this week. Producer prices rose 1.4% in April, more than double the 0.5% economists expected, pushing the year-over-year reading to 6% (Source: Bureau of Labor Statistics). Even after removing volatile categories like food and energy, producer costs rose 1% in a single month and are now running at 5.2% year over year.

Consumer inflation, as measured by Consumer Price Index (CPI), is currently running at 3.8% year over year (Source: Bureau of Labor Statistics). The gap between what producers are paying and what consumers are being charged is 2.2 percentage points. That gap has a name. Economists call it pipeline pressure. In practical terms, this means businesses absorb rising costs for a while, but eventually many pass them through to consumers. A more direct description: the bill hasn’t arrived yet.

The gap between producer prices (6.0%) and consumer prices (3.8%) has reopened to 2.2 percentage points — a level historically associated with upward pressure on consumer inflation over the following two to four months.

What the Gap Tells Us

What the Gap Tells Us

PPI and CPI do not move in lockstep, but they are connected. Producers bear rising input costs first. Over time, those costs work their way through into the price of manufactured goods, into service charges, into the items that make up the Consumer Price Index. The lag is typically two to four months.

This does not mean we will see a return to 2022 conditions. What it does mean, in our assessment, is that the case for rate cuts in 2026 has weakened materially. In simple terms: markets had been expecting lower interest rates later this year. Wednesday’s report makes that outcome less likely. The Fed already held rates steady at its last meeting. A committee that was divided before that report is unlikely to find consensus for easing rates now. The 10-year Treasury yield will feel this. So will the pricing of risk assets that had quietly assumed lower rates were coming.

Why This Matters for How We Think About Portfolios

The portfolios we manage were not constructed for a world of falling inflation and easy money. They were constructed for a world in which inflation proves stickier than expected, in which government spending continues to push demand into specific sectors, and in which the companies best positioned to absorb or pass through cost pressure are not necessarily the ones that dominate a growth-index fund.

That orientation has been a source of friction in periods when the market has run on AI enthusiasm or rate-cut optimism. It has been a source of stability when the data says something different from what the market was pricing.

Wednesday’s data says something different from what the market was pricing.

The industries we emphasize are not immune to a higher-rate environment. But many operate with long-term contracts, regulated revenue structures, or government-backed demand that makes them less sensitive to the rate cycle than the broader market. A company whose primary customer is the government faces a different set of risks than one whose valuation depends on a multiple that needs falling rates to hold.

The large consumer-facing companies in our portfolios will need to demonstrate that they can pass costs through. The ones we hold have done it before.

The Uncomfortable Honest Answer

The question clients are often too polite to ask directly is whether we saw this coming. The direct answer is: Not this specific report, but yes, the direction.

A year ago, the disinflation narrative was convincing. It had data behind it. We wrote about it. We also noted that PPI had been quietly re-accelerating since mid-2025 while core CPI held relatively steady, and that the gap between the two was rebuilding. We were watching it. Now the gap is measurable enough that Wednesday’s Bureau of Labor Statistics report headline is doing the watching for us.

The question from here is not whether inflation is running hotter than expected. It is how long the pipeline stays full, and whether the Fed has the room to do anything about it. In our assessment, pipeline pressure of this magnitude will prevent meaningful rate cuts for the foreseeable future. Uncertainty remains. What does not change is the discipline behind each portfolio we manage or the need to rethink them every time the data changes.

Questions on this commentary are welcome at info@elevagepartners.com.